Usage-based Insurance

Create valuable engagement with your UBI app users.

Create data-driven dynamic pricing

Keep your policyholders engaged with your app

Coach drivers to reduce risks on the roads

Detect driving events like hard braking and hard accelerations.

Segment your drivers based on their driving behavior.

Detect car crashes in on-device, and get notified immediately.

Promote safer driving behavior through your mobile app.

Get trip details such as time, duration and distance.

Receive detailed crash reports to reduce fraud.

Manage risks by monitoring your users' real-world driving behavior, and detecting events such as harsh braking, hard accelerations, hard turns, and phone handling.

Understand their driving styles with reliable insights.

Reduce loss ratio by coaching your drivers to drive safer. Proven in real-world projects, our digital driver coaching is powered by Sentiance insights and behavioral science.

Accelerate claims processing with our on-device crash detection solution. Investigate your crash claims and reduce fraud with real-world data.

Experience you can rely on

Offering UBI for Insurance Advisors, Online Labels and Insurers.

Understand users’ driving behavior and lifestyle for customer-centric auto insurance.

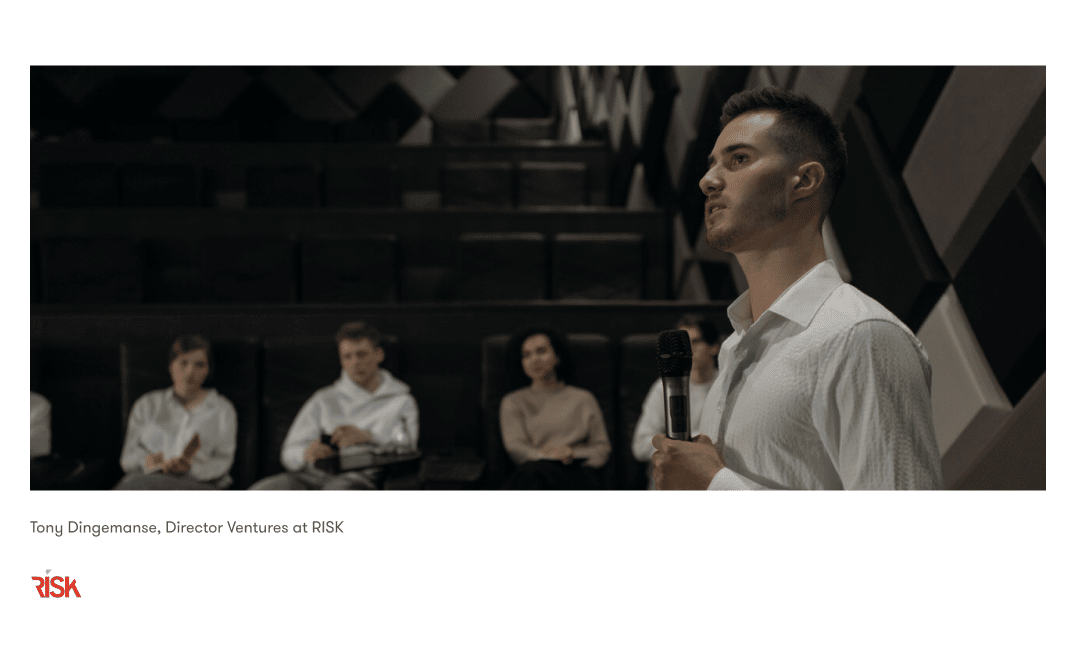

The UK’s first insurer to offer hourly insurance & insurance via app collaborates with Sentiance as technology provider.

Using Behavioral Coaching to create awareness of distracted driving behavior and motivate users to become safer drivers.

World-leading companies trust us with our road safety vision.

Now, it's your turn.

Let's build a safer future together!

Sentiance is the leader in motion insights. Our mission is to save lives every day and shape the future of road safety. Unlike telematics companies, we focus on the driver and not the vehicle because most accidents are caused by human error.

With our revolutionary on-device AI technology, companies use insights from The Edge Platform to produce scalable, cost-efficient, and privacy-centric solutions for their customers.

Subscribe to our newsletter

You may unsubscribe from these communications at any time.

Developed with the support of

| Cookie | Duration | Description |

|---|---|---|

| cookielawinfo-checkbox-analytics | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics". |

| cookielawinfo-checkbox-functional | 11 months | The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional". |

| cookielawinfo-checkbox-necessary | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary". |

| cookielawinfo-checkbox-others | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other. |

| cookielawinfo-checkbox-performance | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance". |

| viewed_cookie_policy | 11 months | The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data. |